The Reality of Rent Cashflow Tokens

Rent cashflow tokens promise passive income by slicing rental properties into digital shares, but the model faces structural constraints that separate marketing from reality. While the underlying assets are physical homes, the returns are governed by on-chain mechanics, legal wrappers, and market liquidity that traditional landlords never face.

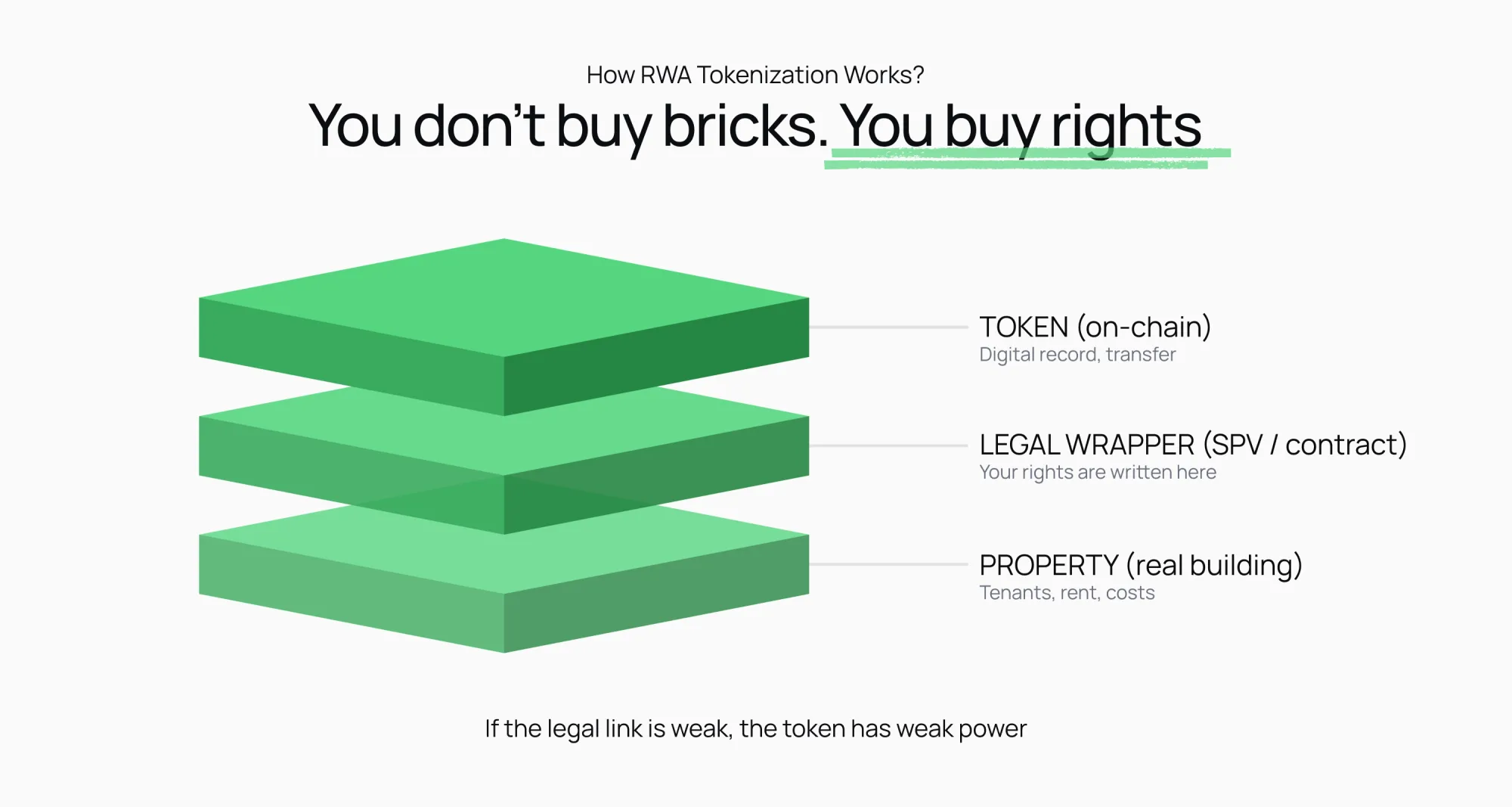

The primary constraint is the legal structure. Most tokens represent interests in a Special Purpose Vehicle (SPV) that owns the property, not the property itself. This means your cashflow is subject to the SPV’s expenses, management fees, and potential legal disputes. If the SPV fails or the property manager underperforms, the token value drops regardless of the building’s physical condition. You are exposed to counterparty risk that doesn’t exist when you hold a deed directly.

Liquidity is the second major hurdle. Unlike stocks, rent cashflow tokens often trade on secondary markets with thin volume. You may face wide bid-ask spreads or difficulty exiting your position quickly. This illiquidity premium is often baked into the token price, reducing your effective yield. If you need to sell during a market downturn, you might accept a significant discount, turning a paper gain into a realized loss.

Finally, the "2% rule" and other traditional metrics don’t always apply cleanly. Tokenized properties may have higher operational costs due to technology infrastructure and regulatory compliance. A property that looks profitable on paper might deliver lower net cashflow once these on-chain and legal fees are deducted. Always verify the net operating income (NOI) after all fees, not just the gross rent.

Rent cashflow tokens choices that change the plan

Use this section to make the Rent Cashflow Tokens decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

How to Choose the Right Rent Cashflow Tokens

Tokenized real estate offers liquidity, but not every token is built for steady income. The difference between a high-yield rental token and a speculative flip token comes down to structure. You need a framework that separates marketing hype from actual cash flow mechanics.

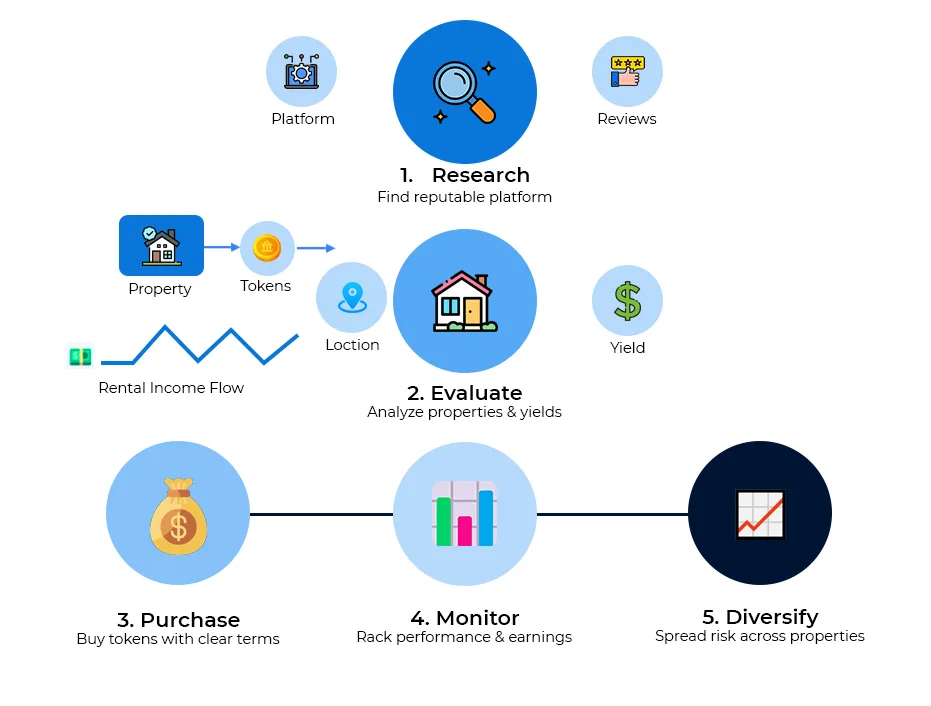

Use these steps to evaluate any rent cashflow token before committing capital.

Look for a Special Purpose Vehicle (SPV) that holds the deed. The token should represent a direct ownership share in the LLC that owns the property, not a derivative contract. This legal structure ensures that rental income flows through to token holders via smart contracts, rather than relying on a third-party promise to pay.

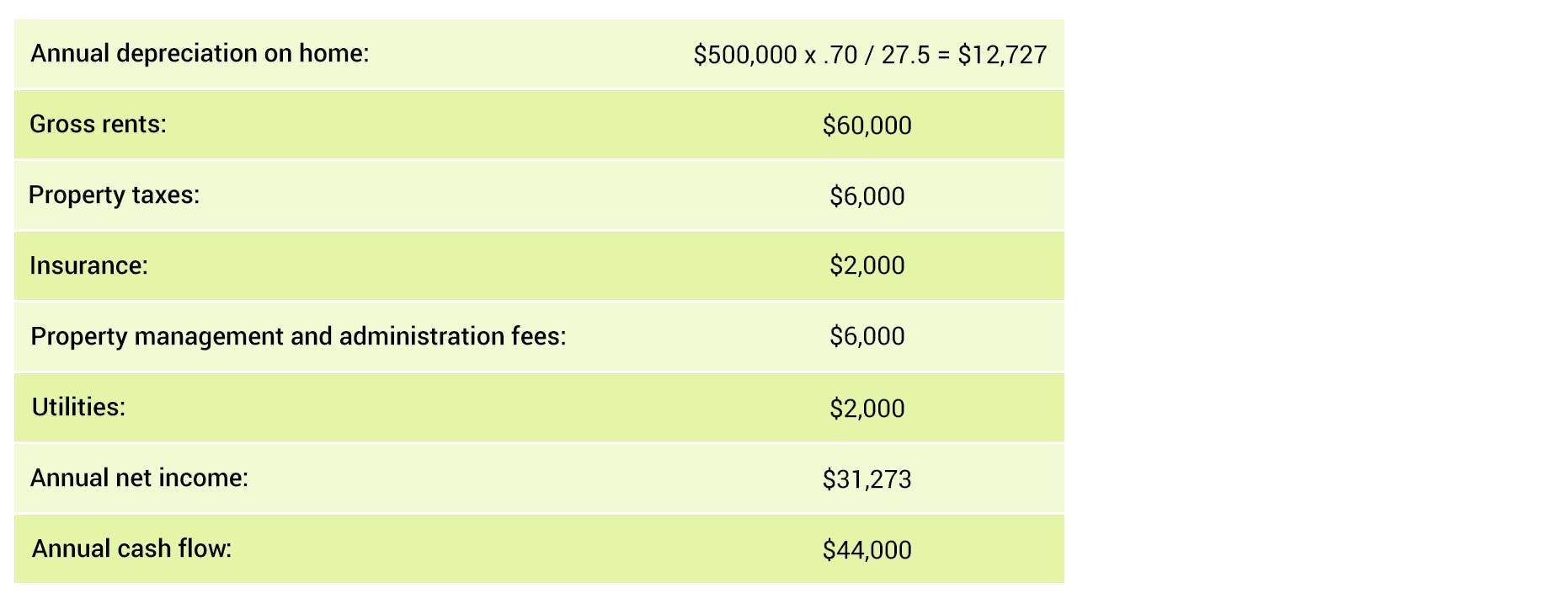

Cash flow is not just revenue. Subtract operating expenses (taxes, insurance, maintenance, property management) from gross rent to find the NOI. A healthy rent cashflow token should show an NOI margin of at least 20-30%. If the token promises high yields but the underlying property has thin margins, the risk of default or dilution increases significantly.

The 2% rule is a standard heuristic: monthly rent should equal or exceed 2% of the purchase price. For example, a $200,000 property should rent for $4,000/month. While this rule is less common in high-cost markets, it serves as a useful baseline. If the tokenized property fails this test, the cash flow potential is likely too low to cover the token platform’s fees and investor returns.

Reliable rent cashflow tokens distribute income monthly or quarterly. Review the platform’s track record. Do they have a history of consistent distributions? Irregular payments often signal property management issues or cash flow gaps. Avoid tokens that promise annual distributions, as this aligns more with equity appreciation than rental income.

How do you sell your tokens? Check the secondary market liquidity. Some platforms have built-in buyback programs or partnerships with exchanges. Others rely on you finding a private buyer. A clear exit path is critical; otherwise, you may be locked into the property for years, defeating the purpose of tokenization.

As an Amazon Associate, we may earn from qualifying purchases.

Spotting Misleading Claims and Weak Options

Tokenized real-world assets (RWAs) promise liquidity and fractional ownership, but the space is still maturing. Investors often encounter projects that overstate returns or understate risks. Understanding the difference between a robust cash flow model and a marketing gimmick is essential before committing capital.

The 2% Rule: A Quick Filter, Not a Guarantee

The 2% rule suggests monthly rent should equal or exceed 2% of the purchase price. For a $100,000 property, this means $2,000 in monthly rent. While this metric helps quickly screen for strong cash flow potential, it is rarely achievable in high-cost urban markets today. Relying solely on this rule can lead you to overlook properties with solid fundamentals in appreciating markets. Use it as an initial filter, not a final decision tool.

Cash Flow Targets: Beyond the Surplus

A good cash flow occurs when rental income covers all expenses and provides a monthly surplus. Many investors target $100 to $200 per unit, but this varies by market and goal. Tokenized projects often project high yields based on optimistic occupancy rates or low vacancy assumptions. Scrutinize the underlying property’s actual cash flow history. If the tokenized share relies on projected rather than realized cash flow, the risk increases significantly.

Watch for Hidden Fees and Illiquidity

Tokenized assets may appear liquid, but secondary markets are often thin. High management fees, platform fees, or exit penalties can erode returns. Always check the tokenomics. If the fee structure is complex or opaque, it is a red flag. Compare the net yield after all fees against traditional real estate investment trusts (REITs) or direct ownership to ensure you are getting fair value.

No comments yet. Be the first to share your thoughts!