What rent cashflow tokens actually are

Rent cashflow tokens represent a specific slice of real estate finance: the right to receive rental income from a property, rather than ownership of the building itself. This distinction matters because it isolates the yield generation from the underlying asset's appreciation or depreciation. When you buy a traditional REIT or a direct property deed, you are exposed to the full cycle of real estate value. Cashflow tokens strip that away, offering a pure play on the net operating income (NOI) of the underlying asset.

Think of these tokens like a bond backed by a lease agreement. The issuer collects rent from tenants, pays property management fees, covers maintenance, and services any debt on the property. The remaining cash is distributed to token holders, typically on a monthly or quarterly basis. This structure transforms illiquid real estate income into a liquid, tokenized stream. It is not equity; you do not vote on property management decisions, nor do you benefit if the property value doubles. You only benefit if the tenants pay rent on time.

This model appeals to investors seeking predictable yield without the operational headaches of landlordship. However, it also introduces unique risks. If the property becomes vacant or the tenant defaults, the cashflow stops. Unlike a diversified REIT that spreads risk across hundreds of properties, many cashflow token offerings are tied to single assets or small portfolios. This concentration risk means the performance of your token is directly tied to the specific property's ability to generate rent.

To understand the mechanics, it helps to look at how traditional cashflow analysis works. In conventional real estate, you calculate cash flow by subtracting all operating costs and debt service from total rental income. Rent cashflow tokens automate this distribution process. The smart contract or special purpose vehicle (SPV) handling the asset executes these calculations and distributes funds programmatically. This transparency is a key feature, as investors can often track the underlying property's performance metrics in real-time through the platform hosting the token.

The primary value proposition of rent cashflow tokens is accessibility and liquidity. Traditional real estate income requires significant capital to enter and is difficult to exit quickly. Tokenization lowers the minimum investment threshold, allowing smaller investors to participate in high-yield commercial or residential leases. It also creates a secondary market where these income streams can be traded, providing an exit route that traditional real estate investors rarely have. For those analyzing rent cashflow tokens, the focus shifts entirely from property appreciation to the stability and growth of the underlying rental income.

The onchain infrastructure behind the yield

Rent cashflow tokens analysis reveals that the value of these instruments rests entirely on the reliability of the data feeding them. Unlike traditional real estate, where ownership is recorded in county clerks' offices, tokenized rental income depends on a digital chain of custody. This chain must bridge the physical world of lease agreements with the immutable logic of smart contracts. If the data entering the system is flawed, the yield distributed to token holders is equally compromised.

The process begins with off-chain verification. Rental property cash flow analysis traditionally involves subtracting operating costs and mortgage payments from gross income to determine net operating income. In a tokenized model, this calculation is not manual. Specialized oracles aggregate data from property management software, bank statements, and tenant payment histories. These oracles act as the bridge, translating real-world cash flow into on-chain signals. They verify that rent was paid, repairs were authorized, and expenses were covered before triggering any on-chain events.

Once verified, the data feeds into smart contracts that automate distribution. These contracts are programmed to split incoming rental payments according to a predefined waterfall structure. Senior tranches receive their share first, followed by mezzanine and equity layers. This automation removes the administrative friction of traditional REITs, allowing for near-instant yield distribution. However, it also means the contract is only as good as the legal wrapper ensuring the underlying property rights are enforceable. Without robust legal structures backing the token, the code is just an empty ledger.

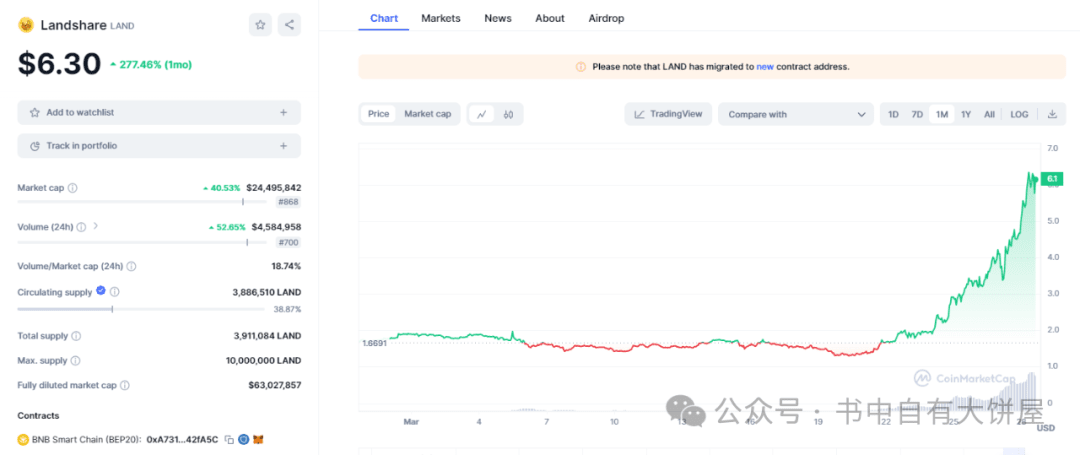

To understand how this infrastructure performs in the broader market, it helps to look at the performance of related real-world asset (RWA) indices. The following chart illustrates the price action of a leading RWA-focused token, providing context for how investors are valuing the underlying infrastructure.

Comparing rent cashflow token platforms

The landscape of rent cashflow tokens analysis reveals distinct approaches to fractional real estate ownership. While the underlying asset—residential or commercial rental property—remains consistent, the mechanisms for yield distribution, investor entry, and regulatory protection vary significantly. Selecting a platform requires evaluating how these structural differences impact your actual return on investment and risk exposure.

Platform Comparison

The following table contrasts the operational models of four prominent platforms in the fractional rental market. These metrics highlight the trade-offs between liquidity, yield potential, and regulatory safeguards.

| Platform | Min. Investment | Yield Source | Jurisdiction | Liquidity |

|---|---|---|---|---|

| RealNex | $25,000 | Rental Income + Appreciation | US (SEC Reg D) | Secondary Market |

| Lofty AI | $50 | Rental Income (USDC) | US (SEC Reg S) | Secondary Market |

| Hoose | $100 | Rental Income (STABLE) | US (SEC Reg D) | Secondary Market |

| Blockshelter | €50 | Rental Income (EUR) | EU (MiCA Compliant) | Secondary Market |

Yield Mechanics and Asset Quality

Yield in rent cashflow tokens analysis is primarily driven by the net operating income (NOI) of the underlying properties. Platforms like Lofty AI and Hoose offer lower barriers to entry but often focus on specific geographic markets with higher rental yields to compensate for platform fees. RealNex targets accredited investors with larger minimums, typically offering properties in markets with stronger long-term appreciation potential alongside stable cash flow.

It is critical to examine the debt structure. Platforms that use leverage (mortgages) on the underlying properties may offer higher cash-on-cash returns but introduce interest rate risk. Platforms that offer equity-only investments provide lower yields but eliminate the risk of foreclosure due to debt service shortfalls.

Regulatory Compliance and Investor Protection

Regulatory jurisdiction dictates the level of investor protection. US-based platforms like RealNex, Lofty AI, and Hoose operate under SEC regulations (Reg D or Reg S), which impose strict disclosure requirements and accreditation checks. European platforms like Blockshelter must comply with MiCA (Markets in Crypto-Assets Regulation), which provides a standardized framework for tokenized assets within the EU.

For investors, this means verifying the platform's legal structure. Tokens issued under Reg D are generally restricted to accredited investors, limiting liquidity but ensuring rigorous due diligence. Tokens issued under Reg S or MiCA may be available to non-accredited investors but often come with stricter holding periods and secondary market restrictions.

Yield sustainability under pressure

The Rent Cashflow Tokens analysis must account for the fact that these assets do not exist in a vacuum. They are tethered to the broader real estate cycle and the cost of capital. When interest rates rise, the cost of servicing the underlying mortgages increases, directly squeezing the net operating income. This sensitivity means that yield projections based on low-rate environments are often optimistic. Investors need to stress-test their models against higher financing costs to understand the true downside risk.

Market cycles also play a pivotal role in yield stability. During periods of economic contraction, vacancy rates tend to rise, and tenants may struggle to meet rent obligations. This creates a dual pressure: lower rental income and higher collection costs. The Rent Cashflow Tokens analysis should therefore prioritize assets in markets with diversified economic bases and strong population growth. These areas are more likely to maintain occupancy levels even during downturns, providing a buffer against yield compression.

Yield compression is a real risk as capital flows into the space. As more investors chase the same underlying assets, property prices rise, which drives down the initial cash-on-cash return. To counter this, the strategy must focus on operational efficiency and value-add opportunities. This might include renovating units, reducing operating expenses, or implementing dynamic pricing models. By actively managing the underlying real estate, the tokenized structure can maintain attractive yields even as market dynamics shift.

How to evaluate a rent cashflow token

Before allocating capital, you need to strip away the marketing gloss and look at the underlying mechanics. Rent cashflow tokens are only as stable as the legal structures and data feeds powering them. Treat this evaluation like a traditional commercial real estate audit, but with a sharper focus on code and compliance.

Check if the token is backed by a specific SPV (Special Purpose Vehicle) or trust. The legal document must explicitly state that token holders have a claim on the rental income or the underlying property. Without a clear legal path from the blockchain to the landlord, your yield is just a promise, not an asset.

Oracles bridge off-chain rent payments to on-chain smart contracts. If the oracle fails to update, yield distribution stops or becomes inaccurate. Look for decentralized oracle networks or multi-signature verification processes that prevent a single point of failure in payment reporting.

High yields often mask high vacancy risks. Review the property’s historical occupancy rates and the creditworthiness of the tenants. A tokenized asset tied to a single, unstable tenant is far riskier than a diversified portfolio with long-term leases. Calculate the net operating income (NOI) after accounting for realistic vacancy buffers.

Don’t just look at the current APY. Model how the yield changes if interest rates rise, maintenance costs increase, or property values dip. Use the capitalization rate to gauge if the token is priced correctly relative to its income-generating potential.

A disciplined due diligence process separates speculative tokens from viable income assets. By verifying the legal wrapper, ensuring oracle reliability, and stress-testing tenant quality, you protect your capital against the structural risks inherent in tokenized real estate.

Common questions about tokenized rent

Tokenized rent transforms physical property rights into digital assets, but the mechanics differ significantly from traditional real estate investing. Understanding the specific liquidity constraints, tax implications, and yield distribution methods is essential for accurate rent cashflow tokens analysis.

No comments yet. Be the first to share your thoughts!