What rent cashflow tokens actually are

Rent cashflow tokens are digital shares in real estate assets that distribute rental income directly to holders. Unlike general real-world asset (RWA) tokens, which might represent ownership in a single building or a vague real estate fund, these specific instruments are engineered for one purpose: passing through the monthly net operating income generated by the underlying property.

The mechanism is straightforward. A property is placed in a legal entity, typically a Special Purpose Vehicle (SPV). That entity issues tokens on a blockchain, each representing a fractional percentage of the ownership. When tenants pay rent, the funds are collected, operating expenses are paid, and the remaining net cashflow is distributed to token holders, usually on a monthly or quarterly basis. This creates a direct, automated link between offchain rental activity and onchain wallet balances.

This structure distinguishes rent cashflow tokens from stablecoins. Stablecoins are pegged to fiat currencies like the US dollar and derive their value from reserve assets, not from the performance of a specific physical asset. Rent cashflow tokens, conversely, derive their value and yield from the real estate market itself. Their price fluctuates based on property valuation, occupancy rates, and rental demand, while their yield is tied to the actual cash generated by the building.

By removing the traditional barriers to entry, such as large down payments and complex property management logistics, these tokens allow investors to access real estate yields with the liquidity of a crypto asset. You are not just buying a piece of a building; you are buying a stream of income, tokenized for efficiency and transparency.

The trust layer behind tokenized rent

Tokenized rent is only as reliable as the systems that feed it data. If the underlying rental performance is opaque, the token becomes a speculative asset rather than a yield instrument. The infrastructure stack bridges the gap between physical leases and digital ledgers through three main components: legal structures, smart contracts, and oracles.

Legal SPVs and Real-World Assets

Before a single token is minted, the physical property must be isolated from the broader market. This is typically done through a Special Purpose Vehicle (SPV), a legal entity created solely to hold the real estate asset. The SPV owns the property, collects the rent, and pays the expenses. This structure ensures that if the property manager or the originator of the token goes bankrupt, the underlying real estate remains safe and separate from other liabilities.

Smart Contracts for Distribution

Smart contracts automate the distribution of cash flow. Instead of waiting for a quarterly statement, the contract is programmed to send pro-rata shares of the rent directly to token holders’ wallets. This reduces administrative overhead and eliminates the risk of human error in payments. The contract acts as a neutral escrow, ensuring that every dollar of net operating income is distributed according to the token’s terms.

Oracles for Data Integrity

Oracles are the data pipelines that connect the blockchain to the real world. They verify that the rent was actually paid and that the property conditions haven’t deteriorated. Without reliable oracles, the token price would drift away from the actual value of the underlying asset. They provide the "trust" layer by confirming that the on-chain data matches the off-chain reality.

Market Correlation

While the internal mechanics ensure yield accuracy, the token’s market price still reacts to broader financial conditions. Understanding how these assets correlate with traditional markets is essential for risk management.

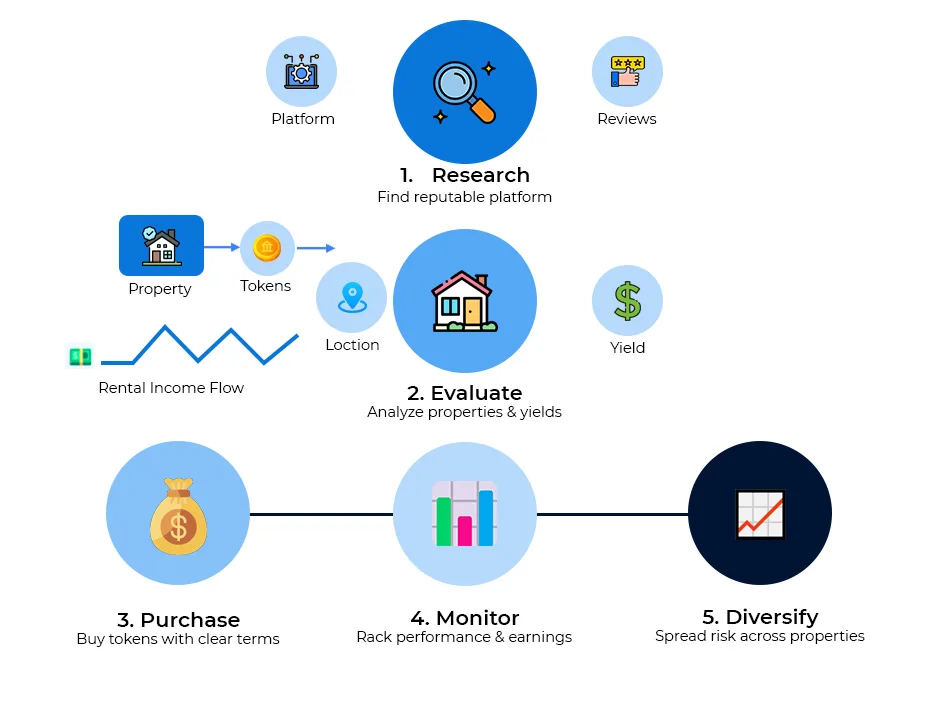

Comparing Top Rent Cashflow Token Platforms

Choosing the right platform is the first step in building a functional rent cashflow token portfolio. Not all platforms are created equal; they differ significantly in how they handle legal structures, investor access, and secondary market liquidity. This comparison focuses on three distinct approaches: RealT’s direct property ownership model, Propy’s broader real estate transaction infrastructure, and Tokeny’s issuer-focused framework for regulated securities.

Platform Comparison

The table below breaks down the key operational differences. Note that yield and liquidity metrics are dynamic and depend on the underlying asset pool and market conditions at the time of purchase.

| Platform | Legal Model | Min. Investment | Liquidity Source | Primary Jurisdiction |

|---|---|---|---|---|

| RealT | LLC Ownership | $50 | Internal Marketplace | US (Wyoming/Delaware) |

| Propy | Tokenized Deed/Security | Varies | Partner Exchanges | Global (US/EU) |

| Tokeny Issuers | Regulated Security Token | Varies (Institutional) | Secondary Marketplaces | EU (France/Germany) |

Key Trade-offs

RealT is often the entry point for retail investors because of its low barrier to entry and transparent, US-based LLC structures. Each token represents a direct share in a property-owning LLC, making the legal path from token to rent straightforward. However, liquidity is limited to RealT’s internal marketplace, which can mean longer holding periods if you need to exit quickly.

Propy focuses on the entire transaction lifecycle, from title transfer to tokenization. This makes it a robust infrastructure provider, but for individual investors, the experience can be more complex. Propy often partners with other issuers, meaning the specific legal wrapper and liquidity options depend on the particular token offering you choose.

Tokeny is less of a consumer-facing platform and more of a technology provider for issuers of regulated security tokens. If you are investing through a Tokeny-powered offering, you are likely dealing with strict investor accreditation requirements (especially in the EU) and higher minimum investments. The upside is often access to institutional-grade real estate assets with higher regulatory scrutiny.

Choosing Your Provider

If you are new to tokenized real estate, RealT offers the most straightforward path to understanding how cashflow works. For investors looking for broader geographic diversification or institutional assets, exploring Propy or Tokeny-backed offerings may be appropriate, but always verify the specific legal structure and liquidity terms of each individual token.

As an Amazon Associate, we may earn from qualifying purchases.

Tools for accurate cashflow analysis

You cannot rely on intuition when tokenizing real estate. Rent cashflow tokens analysis requires precise data integration across onchain ledger entries and offchain property metrics. The best tools bridge this gap, allowing you to verify that the rent coming in matches the distributions going out.

Dashboards and Oracle Feeds

Onchain data is transparent but fragmented. You need a dashboard that aggregates transaction history from multiple blockchains. Look for platforms that pull directly from the token contract’s event logs. This ensures you are seeing actual rent payments, not just token transfers.

Oracle feeds are equally important. They bring offchain rental income data into the blockchain. Reliable oracles verify that the landlord has collected rent before triggering a distribution. Without this verification layer, the token’s yield is just a promise, not a backed asset. Always check if the oracle provider has a proven track record in real estate data.

Traditional Calculators Adapted for Crypto

Even with perfect data, you need to model scenarios. Traditional real estate calculators like DoorLoop or CashflowCalc are excellent starting points. They handle standard metrics like operating expenses and mortgage payments. However, you must adjust them for crypto-specific factors.

Add costs for gas fees, oracle data subscriptions, and smart contract audit fees. These are often ignored in standard spreadsheets but significantly impact net yield. Use these adapted calculators to stress-test your investment. If the token underperforms when you factor in blockchain overhead, it is likely a poor investment. Pair this with a live PriceWidget to see how token price volatility affects your overall return.

Strategy for evaluating onchain real estate yield

Evaluating rent cashflow tokens requires treating on-chain yields differently than traditional real estate. You are not just buying property; you are buying a digital claim on that property’s income stream, exposed to both real-world operational risks and crypto market volatility. A high nominal yield often masks underlying risks like smart contract vulnerabilities or tenant vacancy.

To navigate this, use a structured framework that separates the real estate fundamentals from the token mechanics. This approach helps you distinguish between a genuinely profitable asset and a yield trap driven by speculative token demand.

Start with the property, not the token. Calculate the net operating income (NOI) by subtracting operating expenses and debt service from gross rental income. If the underlying property does not cash flow positively in traditional terms, the token will not either. Use standard rental property cash flow analysis tools to verify that the rent covers all costs and still leaves a surplus.

On-chain yields are rarely distributed 1:1 to investors due to platform fees, gas costs, and smart contract risks. Subtract these operational frictions from the gross yield. Additionally, consider the liquidity premium: can you sell your tokens quickly without a significant price impact? Illiquid tokens often require a higher yield to compensate for the difficulty of exiting the position.

Real estate rents are sticky, but token prices are not. A 10% APY yield can be wiped out if the token price drops 20% in a month. Model your returns in stablecoin terms rather than native token terms. If the yield is paid in a volatile asset, hedge that exposure or assume a lower effective yield to account for potential depreciation of the payout token.

Do not concentrate your exposure in a single property or protocol. Spread investments across different real estate markets to mitigate local economic downturns. Simultaneously, diversify across tokenization platforms to reduce counterparty risk. If one platform experiences a technical failure or regulatory issue, your entire portfolio should not be compromised.

| Factor | Traditional RE | On-Chain Tokens |

|---|---|---|

| Liquidity | Low (months to sell) | High (instant settlement) |

| Yield Transparency | Quarterly reports | Real-time on-chain data |

| Volatility Exposure | Low (price stable) | High (token price fluctuates) |

| Minimum Investment | High (down payment) | Low (fractional shares) |

The chart above shows the volatility of a traditional equity benchmark. While real estate rents are stable, the tokenized claim on those rents trades like a tech stock. This divergence is the core risk in rent cashflow tokens: you earn steady rent but hold a volatile asset. Always calculate your return in stablecoins to see the true picture.

Frequently asked questions about tokenized rent

How do I calculate cash flow for rent tokens?

The math mirrors traditional real estate: subtract total operating costs and mortgage payments from the rental income. For tokenized assets, you must also account for platform fees and blockchain network costs. The Internal Rate of Return (IRR) remains the standard metric for measuring annual growth, but it only reflects projected performance based on historical data.

Is there liquidity for rent cashflow tokens?

Liquidity depends entirely on the secondary market infrastructure supporting the token. Unlike physical property, which can take months to sell, tokens can theoretically be traded instantly if buyers are present. However, many platforms lack deep order books, meaning you may face wide bid-ask spreads or inability to exit during market stress. Always check the specific platform’s trading volume before investing.

How are rent tokens taxed?

Tax treatment varies by jurisdiction but generally follows capital gains or ordinary income rules depending on how the token is structured. Dividends from rent payments are typically taxed as income in the year received. If you sell the token for a profit, it may trigger capital gains tax. Consult a tax professional familiar with digital assets, as regulations are evolving rapidly and differ significantly between countries.

Are rent cashflow tokens secure?

Security relies on the underlying blockchain and the smart contract auditing process. Reputable platforms use audited code to prevent exploits, but no system is immune to hacking or coding errors. Additionally, custodial risks exist if the platform holds the underlying property deeds or funds. Look for platforms with insurance coverage and transparent security audits to mitigate these risks.

No comments yet. Be the first to share your thoughts!