What rent cashflow tokens actually are

Rent cashflow tokens represent a shift from physical property ownership to digital claims on real estate income streams. This analysis compares that infrastructure against traditional direct ownership and REITs to determine where the yield actually comes from and what risks remain.

Yield mechanics: Onchain vs traditional

The core difference in a Rent Cashflow Tokens analysis comes down to how value is stripped away before it reaches the investor. Traditional real estate relies on physical infrastructure—property managers, maintenance crews, and banks—that consumes a significant portion of gross rent. Onchain credit models attempt to compress this layer, but the economics shift rather than disappear. Understanding where the yield originates helps separate infrastructure efficiency from speculative premium.

Direct ownership: The friction of scale

Direct property ownership offers the highest potential gross yield but carries the steepest entry barriers and operational drag. Cash flow is rarely 100% of rent; industry estimates suggest net cash flow often settles between 35% and 60% of gross rent depending on the market and management efficiency (Source: Reddit Real Estate Investing community).

The gap between gross rent and net cash flow is eaten by property taxes, insurance, vacancy reserves, and capital expenditures. While you retain full control, the liquidity premium is low, and the time cost of management is high. Yield is real, but it is labor-intensive.

REITs: Liquidity at a cost

Real Estate Investment Trusts (REITs) offer instant liquidity and diversification but introduce management fees and corporate overhead. Gross yields typically range from 3% to 5%, with net returns often lower after expense ratios. The trade-off is simplicity: you get a check without fixing toilets, but you also get diluted returns from layers of administrative costs.

Rent cashflow tokens: Fractionalization and fees

Tokenized rentals promise higher yields by cutting out the middle management of traditional REITs, replacing it with smart contracts. However, "higher yield" often reflects higher risk or lower quality assets. The fee structure shifts from property management fees to blockchain network fees, smart contract audits, and platform commissions.

While fractionalization lowers entry barriers to near-zero, the net yield must still cover the cost of onchain data verification and offchain property management. The infrastructure is leaner, but the risk profile is distinct.

| Feature | Direct Ownership | Public REITs | Rent Cashflow Tokens |

|---|---|---|---|

| Entry Barrier | High ($50k+ down) | Low ($100+) | Minimal ($10+) |

| Liquidity | Low (Months) | High (Instant) | Medium (Variable) |

| Management Cost | High (Time/Money) | Medium (1-2% fee) | Low (Network/Platform) |

| Typical Net Yield | 4-8% | 3-5% | 5-10%* |

| Primary Risk | Vacancy/Maintenance | Market Volatility | Smart Contract/Regulatory |

*Yields on tokenized assets are often gross or pre-risk-adjusted; net returns vary by protocol.

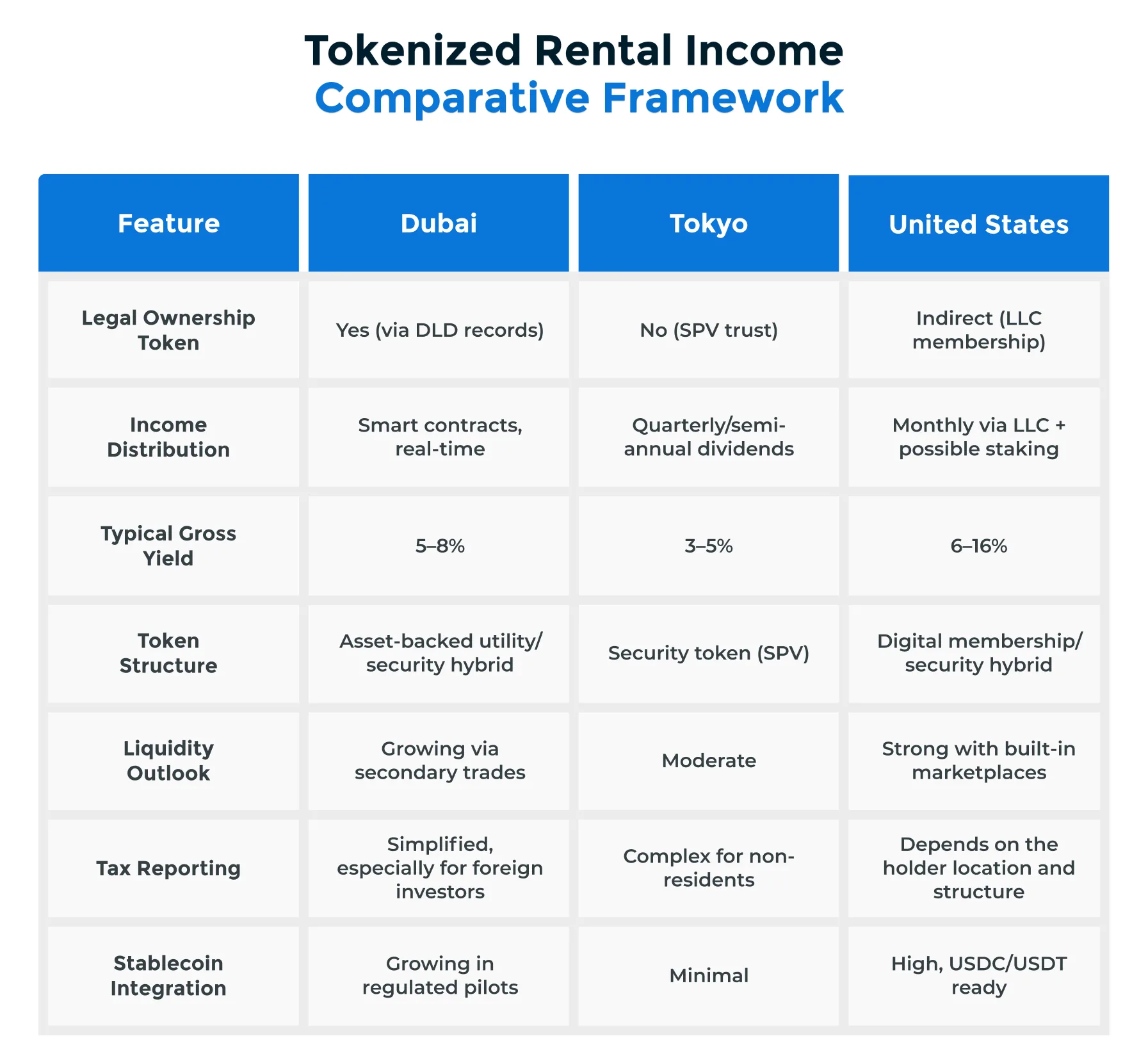

The plumbing behind rent cashflow tokens

Rent cashflow tokens rely on a bridge between physical leases and digital ledgers. This infrastructure translates offchain rent payments into onchain distributions through three layers: legal wrappers, data oracles, and smart contracts. Without this alignment, tokenized real estate remains a speculative asset rather than a yield-generating instrument.

Legal wrappers and SPVs

Most rent cashflow tokens are issued through Special Purpose Vehicles (SPVs). These entities hold the underlying property or mortgage, isolating risk from the issuer. When a tenant pays rent, it flows into the SPV, which then distributes proceeds to token holders. This structure mirrors traditional real estate investment trusts (REITs) but replaces the fund manager with code.

Oracles and data verification

Smart contracts cannot verify rent payments on their own. Oracles act as the bridge, pulling data from property management software or bank accounts to confirm payments. If a tenant defaults, the oracle signals the smart contract to pause distributions or trigger liquidation protocols. This step is critical for maintaining the integrity of the yield.

Smart contract distribution

The final layer is the smart contract, which automates the distribution of cash flows. Once the oracle confirms payment, the contract executes the transfer to token holders' wallets. This process removes the need for manual reconciliation, reducing administrative costs and increasing transparency for investors analyzing rent cashflow tokens.

Risks in tokenized rental income

While Rent Cashflow Tokens analysis often highlights the democratization of real estate investment, the infrastructure carries distinct vulnerabilities that traditional direct ownership does not. Understanding these risks is essential for any investor evaluating on-chain yield.

Smart Contract Vulnerabilities

The code governing token distribution is a single point of failure. A bug in the smart contract can halt yield payments entirely, regardless of whether tenants are paying rent on time. Unlike a traditional landlord who can adjust rents or fix a leak, a contract bug requires a code patch or governance vote. This disconnect means technical risk is separate from property risk.

Warning: Smart contract risk is distinct from property risk. A bug in the distribution contract can halt yield payments regardless of tenant payment status.

Regulatory Uncertainty

The legal status of tokenized real estate remains fluid. If regulators classify these tokens as unregistered securities, platforms may face restrictions or shutdowns. This uncertainty can impact liquidity and the ability to redeem tokens for underlying property value. Investors must assess the jurisdictional framework of the issuing platform before committing capital.

Property Management Failures

Tokenization does not eliminate the need for physical property management. If the underlying property suffers from vacancy, damage, or poor tenant relations, the cash flow backing the tokens diminishes. The token holder has no direct control over these operational decisions, relying entirely on the platform's chosen management team. Poor performance at the property level directly reduces token value.

Liquidity limits to account for

Unlike stocks, tokenized real estate may face thin trading volumes. During market stress, buyers may disappear, making it difficult to exit positions without significant price discounts. This illiquidity trap can lock investors into underperforming assets when they need capital most. Always consider the secondary market depth before investing.

How to evaluate a rent cashflow token

Evaluating a rent cashflow token requires shifting from speculative asset hunting to fundamental property underwriting. The token is just the delivery mechanism; the underlying real estate determines the yield. To perform a proper rent cashflow tokens analysis, you must verify the physical asset's performance, the legal structure's enforceability, and the technology's reliability.

Cap rate (net operating income divided by property value) is the primary indicator of value. Compare the tokenized asset's cap rate against local commercial real estate benchmarks. Ensure the occupancy rate is stable and documented by the property manager, not just projected. A high cap rate often signals high risk or poor management.

Tokens represent shares in a Special Purpose Vehicle (SPV) that owns the property. Verify the SPV's jurisdiction and how it handles foreclosure or default. If the property is in a different country than your residence, understand the legal recourse for dividend distribution and dispute resolution. This structure dictates your actual ownership rights.

Onchain rent payments rely on oracles to bridge off-chain cash flow to on-chain tokens. Review the oracle provider's reputation and data sources. Ensure the smart contract has been audited by a reputable firm. Smart contract bugs or oracle failures can halt dividend distribution, even if the property is performing well.

Unlike traditional real estate, tokens can be sold on secondary markets, but liquidity is not guaranteed. Check the protocol's buyback mechanisms or market maker agreements. Understand the lock-up periods for dividends and any fees associated with selling tokens before the property is sold or refinanced.

A structured checklist helps ensure no critical risk factor is overlooked during your rent cashflow tokens analysis.

Frequently asked questions about tokenized rent

Investors often ask how rent cashflow tokens analysis compares to traditional real estate regarding liquidity, entry costs, and tax treatment. Understanding these mechanics helps you evaluate whether on-chain assets fit your portfolio strategy.

These distinctions highlight why rent cashflow tokens analysis is gaining traction among investors seeking liquidity and transparency.

No comments yet. Be the first to share your thoughts!