What rent cashflow tokens actually are

Rent cashflow tokens are digital representations of ownership in income-producing real estate, but their structure differs significantly from traditional investment vehicles. At their core, these tokens represent a claim on the net operating income of a specific property or a portfolio of properties. When tenants pay rent, that revenue is collected, operating expenses are deducted, and the remaining cash is distributed to token holders, typically on a monthly or quarterly basis. This mechanism transforms illiquid physical assets into liquid, onchain financial instruments.

To understand the distinction, it helps to compare tokenized real estate with Real Estate Investment Trusts (REITs) and direct property ownership. Traditional REITs pool capital to buy large portfolios, offering diversification but limited control and high minimum investment thresholds. Direct ownership provides full control but requires significant capital, management effort, and lacks liquidity. Rent cashflow tokens sit in the middle: they offer fractional ownership, allowing investors to buy small portions of a single property, while the smart contract automates the distribution of profits, reducing administrative overhead.

The primary advantage lies in the transparency and efficiency of the distribution mechanism. In traditional real estate, cash flow calculations can be opaque, relying on quarterly reports and manual bank transfers. With tokenized assets, the underlying property’s financial data is often recorded on a blockchain, and distributions are executed automatically via smart contracts. This reduces the risk of human error and ensures that investors receive their share of the cash flow precisely when the property generates it.

Calculating the actual cash flow from these tokens follows the same fundamental principle as traditional rental properties: income minus expenses. As noted by industry experts, cash flow refers to the net amount of money generated after all operating expenses and debt obligations are paid. For token investors, this means the gross rental income is first used to cover property management fees, maintenance, insurance, and taxes. The surplus, or net operating income, is then distributed to token holders proportional to their ownership stake.

This structure allows for more granular risk assessment. Instead of betting on a broad market index, investors can analyze the specific property backing their tokens. They can evaluate local rental demand, vacancy rates, and tenant quality. However, this also means that the performance of the token is directly linked to the performance of the underlying asset. If the property underperforms, the cash flow distribution will decrease, reflecting the real-world economics of the rental market.

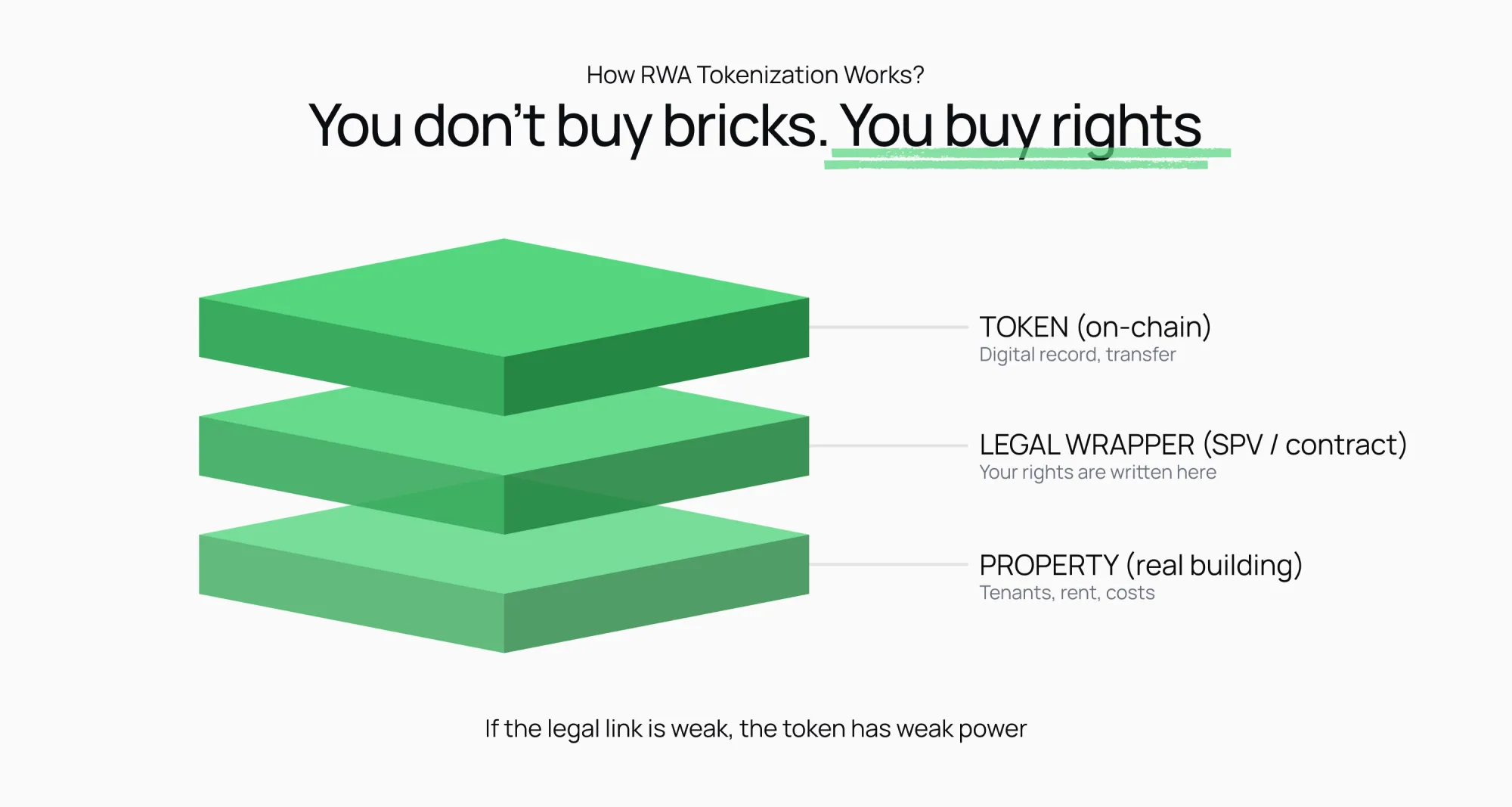

How onchain rent distribution works

The distribution of rent cashflow tokens relies on a predictable sequence of events governed by smart contracts and off-chain legal structures. First, the property manager collects rent and submits expense reports to the Special Purpose Vehicle (SPV) that holds the title. Once the SPV verifies the Net Operating Income (NOI), it instructs the smart contract to calculate each holder's proportional share.

This process eliminates the latency of traditional banking transfers. Instead of waiting for wire processing, distributions are often settled on-chain, allowing investors to see incoming yields in their wallets almost immediately. However, the "onchain" aspect is limited to the distribution ledger; the underlying legal claim to the property remains off-chain, secured by traditional corporate law. Investors must understand that while the code executes the payment, the legal recourse for property disputes remains with the SPV's legal counsel, not the smart contract code.

Top platforms for tokenized real estate

The infrastructure for rent cashflow tokens is moving from experimental pilots to regulated marketplaces. Choosing a platform means evaluating three structural pillars: regulatory compliance, asset quality, and liquidity options. These factors determine whether your tokenized shares represent a secure claim on rental income or a speculative asset with limited exit routes.

We compare the leading providers based on their current operational models. The data below highlights the differences in minimum investment thresholds, yield distribution mechanisms, and secondary market availability.

| Platform | Min. Investment | Yield Type | Regulation | Liquidity |

|---|---|---|---|---|

| RealT | $50 | Monthly Rent | SEC Reg A+ | Secondary Market |

| Lofty AI | $50 | Monthly Rent | SEC Reg A+ | Secondary Market |

| Propy | Varies | Equity/Debt | Varies by Asset | Low |

| RealEstateCrowd | $1,000 | Quarterly Distributions | SEC Reg D | None |

Calculating yield and risk metrics

Evaluating the true return of a rent cashflow token requires looking beyond the advertised Annual Percentage Yield (APY). The headline yield often excludes platform fees, management costs, and potential vacancy periods. A more accurate metric is the Cash-on-Cash Return, calculated by dividing the annual pre-tax cash flow by the total cash invested.

Investors should also assess the Debt Service Coverage Ratio (DSCR) of the underlying property. A DSCR greater than 1.0 indicates that the property generates enough income to cover its debt obligations. For tokenized assets, a DSCR below 1.2 may signal higher risk, as it leaves little margin for error during market downturns. Additionally, consider the platform's fee structure: some charge an upfront acquisition fee (1-5%) and an annual management fee (1-2%), which can significantly erode long-term compounding returns.

Key questions for investors

Tokenized real estate changes how you view cash flow, but the underlying mechanics remain grounded in traditional property metrics. Understanding these benchmarks helps you evaluate whether a specific token offering aligns with your financial goals.

No comments yet. Be the first to share your thoughts!