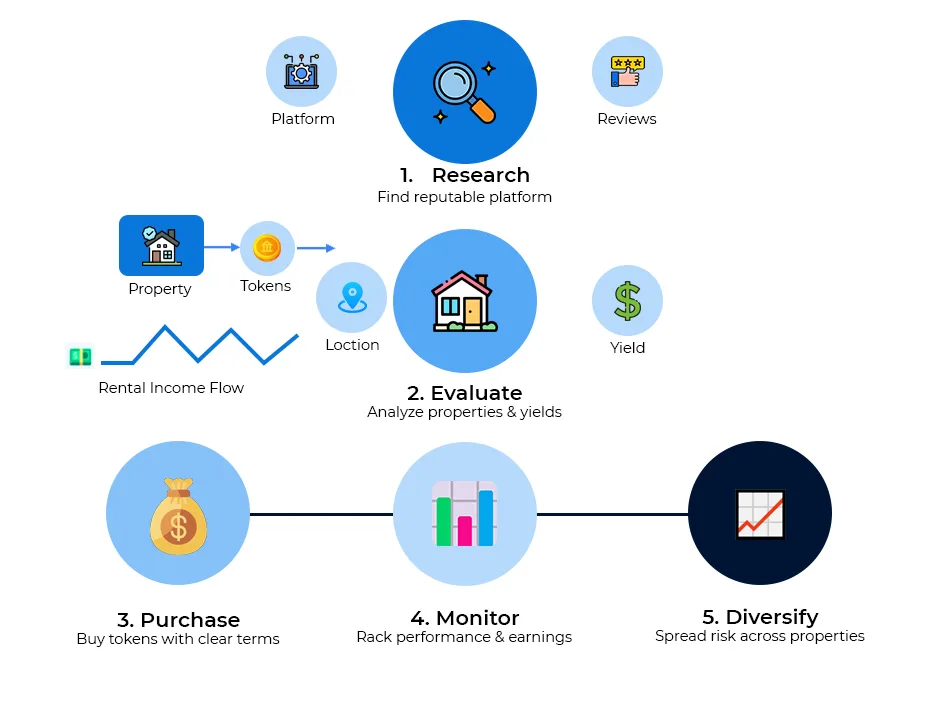

Defining the rent cashflow tokens strategy

The rent cashflow tokens strategy involves fractionalized ownership of income-generating real estate assets, with distributions paid in stablecoins or native tokens. This model digitizes the traditional rental income stream, converting illiquid property equity into liquid, programmable assets on a blockchain network.

Unlike traditional Real Estate Investment Trusts (REITs), which often carry management fees and tax complexities associated with corporate structures, tokenized real estate offers direct exposure to property cash flows. Investors hold digital shares that represent a proportional claim on the underlying asset's rental income. These distributions are typically automated through smart contracts, reducing administrative overhead and increasing the frequency of payouts.

This approach bridges the gap between direct property ownership and public market investing. It lowers the barrier to entry, allowing investors to access high-quality commercial or residential properties with smaller capital commitments. The infrastructure relies on secure token standards and compliant custody solutions to ensure that ownership rights are legally enforceable and transparent.

The traction of this model stems from its ability to solve liquidity issues inherent in real estate. By tokenizing properties, owners can trade shares on secondary markets, providing an exit strategy that traditional real estate lacks. This liquidity premium, combined with the efficiency of automated distribution, makes the rent cashflow tokens strategy a compelling evolution in asset management.

The infrastructure behind tokenized rental income

Tokenizing rental cash flow requires more than just a smart contract; it demands a legal and technical stack that bridges traditional property management with blockchain settlement. The goal is to make the transfer of rent from tenant to investor as automatic as a block confirmation.

Smart contracts for distribution

The core engine is a smart contract that holds the rental income in a stablecoin or native currency. Instead of a landlord manually wiring funds, the contract executes a distribution schedule based on token ownership. This reduces administrative friction and ensures investors receive their share without delay. The contract must be immutable to prevent unauthorized changes to the payout logic.

Oracles for real-world data

Smart contracts cannot see the real world. Oracles act as the bridge, feeding external data into the blockchain. In this context, oracles verify occupancy rates, maintenance costs, and rental income received. This data triggers the contract to release funds or adjust distributions. Without reliable oracles, the tokenized asset would lack the transparency needed for trust.

Legal wrappers for compliance

A smart contract alone has no legal standing. A legal wrapper, typically a Special Purpose Vehicle (SPV), holds the actual property deeds. The tokens represent ownership in the SPV, not the property itself. This structure ensures that investors have legal recourse and that the tokenization complies with securities laws. The SPV handles tenant leases, property taxes, and insurance, while the blockchain handles the financial settlement.

Market volatility and liquidity

The underlying asset is real estate, but the token trades like a crypto asset. This creates a unique risk profile. Investors are exposed to both property performance and crypto market volatility. A technical chart of a relevant RWA token shows how these two markets interact, often with higher volatility than traditional REITs.

This volatility can create entry and exit opportunities but also requires careful risk management. The infrastructure must support high-frequency trading while maintaining the stability of the underlying cash flow.

Tokenized real estate yields vs. traditional assets

Tokenized real estate yields currently sit between 6% and 9% for senior debt strategies, while equity-focused tokens often target 10% to 15% gross returns before fees. These figures generally outperform traditional REITs, which average 4% to 6% total return in recent cycles, and significantly exceed the yield of major crypto assets like Bitcoin, which offers no intrinsic yield.

The primary advantage of tokenization is the elimination of the "illiquidity premium" that traditional private equity real estate demands. In direct rental ownership or non-traded REITs, investors lock up capital for years, expecting higher returns to compensate for the inability to sell quickly. Tokenized assets allow for secondary market trading, compressing this premium and bringing yields closer to public market equivalents.

However, these higher yields come with specific infrastructure risks. Tokenized debt relies on the underlying property's cash flow and the stability of the custodian holding the legal title. Unlike public REITs, which are heavily regulated and audited quarterly, many tokenized offerings operate under private placement exemptions, meaning transparency varies by issuer.

The following table compares the typical yield profiles, liquidity terms, and entry barriers across these investment vehicles.

Evaluating Risks in the Rent Cashflow Strategy

Tokenized real estate offers liquidity, but it does not eliminate the underlying risks of property ownership. In fact, it layers new technical and regulatory complexities on top of traditional market exposure. Understanding these vulnerabilities is essential for protecting capital.

Smart Contract and Infrastructure Risk

The tokenization platform acts as the bridge between physical assets and digital ledgers. If the smart contract governing the token has a vulnerability, or if the custodian holding the physical deed is compromised, the token value can drop to zero regardless of the property's performance. Unlike traditional REITs, where legal recourse is often clearer, smart contract bugs can result in irreversible loss of funds. You are trusting the code and the infrastructure provider as much as the real estate itself.

Regulatory Uncertainty

The legal framework for security tokens is still evolving. Regulations vary significantly by jurisdiction, and changes in securities laws can impact liquidity or even force the delisting of tokens. For example, if a token is deemed an unregistered security in a major market, trading volume can evaporate overnight. Investors must ensure the token issuer is compliant with local regulations, such as those enforced by the SEC in the United States, to avoid legal entanglements that could freeze assets.

Real Estate Market Exposure

Tokenized rent cashflow remains tied to the physical real estate market. If rental incomes decline due to economic downturns, vacancies, or rising maintenance costs, the cash distributions to token holders will decrease. This is not a theoretical risk; historical data shows that property values and rental yields fluctuate with interest rates and local economic conditions. The token price will reflect these changes, meaning you are still exposed to the cyclical nature of real estate.

Building a rent cashflow tokens checklist

Before committing capital to tokenized real estate, you need a rigorous due diligence framework. Unlike traditional REITs, tokenized platforms introduce specific technological and structural risks that require verification. This checklist ensures you evaluate the underlying infrastructure, legal protections, and yield sustainability before investing.

Confirm the legal entity holding the property. Is it a Delaware LLC, a Singapore VCC, or another jurisdiction? Check if the token represents direct equity in the LLC or a security token offering (STO) compliant with local securities laws. The legal wrapper dictates your rights and enforcement capabilities.

Rent distributions rely on oracles to translate off-chain cash flows into on-chain token transfers. Verify which oracle provider is used (e.g., Chainlink) and how often data is updated. Ensure there is a fallback mechanism if the oracle fails, as this directly impacts your ability to receive yield.

Identify the property management company. Is it a reputable local firm or a subsidiary of the token platform? Analyze the historical occupancy rates and net operating income (NOI) of the underlying asset. High yields often correlate with higher vacancy risks or poor management.

Tokenized real estate is inherently illiquid. Determine if the platform offers a secondary market for trading tokens. If so, what are the trading fees, minimum holding periods, and buyer verification requirements? Without a clear exit strategy, your capital is locked until the property is sold or refinanced.

Ensure the platform’s smart contracts have been audited by a reputable firm (e.g., CertiK, OpenZeppelin). Look for the audit report and check for any critical vulnerabilities that were not patched. Unaudited contracts pose a significant risk of exploitation or bugs that could freeze your assets.

This checklist provides a baseline for evaluating rent cashflow tokens. Always conduct your own research and consult with a financial advisor before making investment decisions in this emerging asset class.

No comments yet. Be the first to share your thoughts!